Compliance as Operating System: How Gate.io Built Four Different Market Entries

Most cryptocurrency founders treat regulation as a ceiling. The exchanges that crossed into mainstream finance treated it as the operating layer they had to build on, not the obstacle they had to route around.

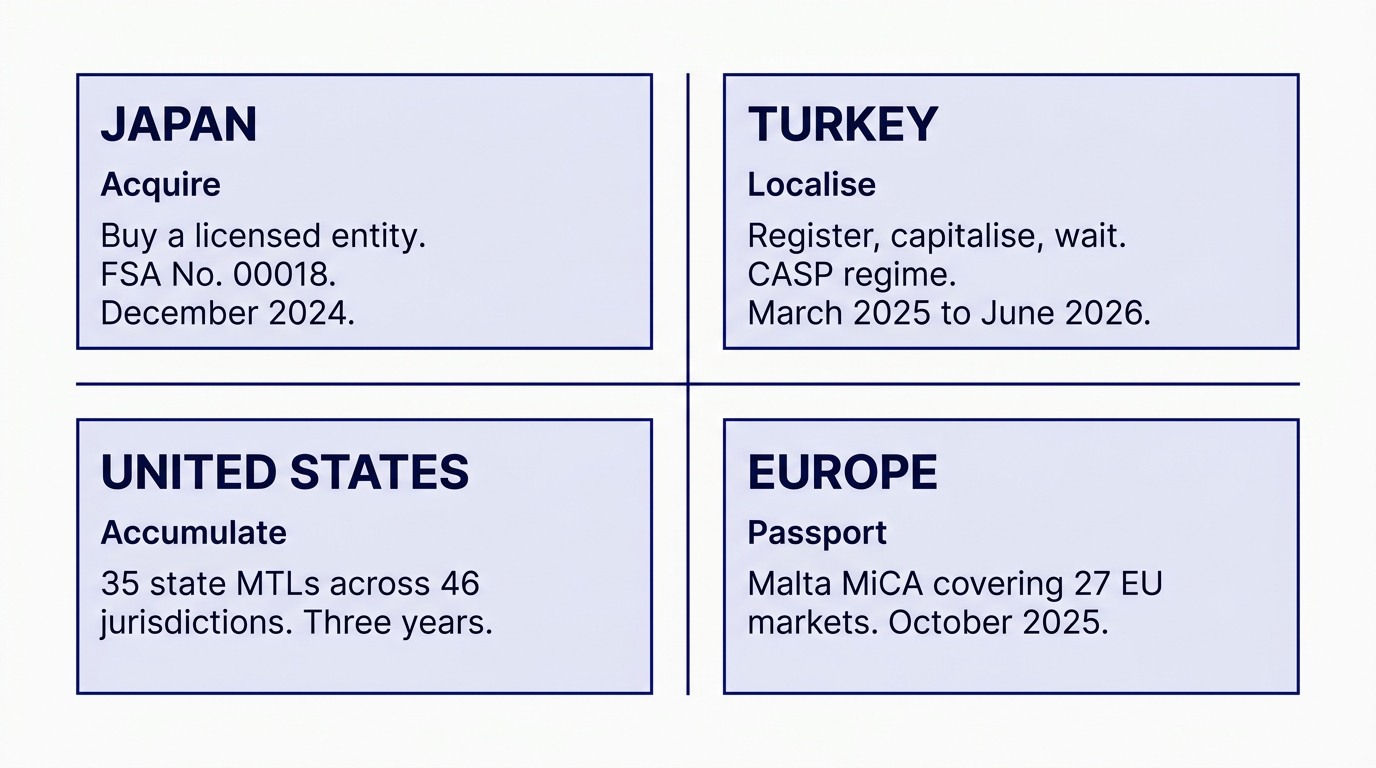

Gate.io is the clearest published example of this distinction. Between 2018 and 2026, Gate Group built four structurally different market entry mechanisms across the United States, Japan, Turkey, and the European Union. Each market got a different entity, a different licence, and a different operating model. The corporate parent functions as the connecting layer above all four. Each subsidiary is engineered to be native to its market.

A disclosure first: I worked at Gate.io previously and currently serve as General Manager of PEPS Ventures Berhad, where I oversee product and regulatory strategy for three Malaysian property fintech products. This piece is informed by direct exposure to how the compliance function operated during Gate's early licence accumulation years, then crosschecked against current public filings.

The Japan Move: Acquire a Licensed Entity

The question every foreign crypto exchange asks about Japan is: should we apply for a Financial Services Agency (FSA) registration ourselves, or should we acquire a Japanese entity that already has one?

Japan's crypto licensing regime is one of the highest barrier in the world. The FSA expects a Japanese corporate entity, Japanese senior management, capital adequacy, segregated custody, and AML systems calibrated to Japanese standards. Greenfield applications have historically taken three to five years with uncertain outcomes. Most foreign applicants either withdraw or are quietly rejected.

In July 2024, Gate.io announced it would stop accepting new accounts from Japanese residents and wind down its global services to Japan. The announcement read like a regulatory exit. It was not. On 24 December 2024, Gate Group, through Gate Japan K.K., completed the acquisition of all issued shares of Coin Master Co., Ltd., a JFSA-registered Japanese crypto exchange business operator holding FSA registration number 00018. The acquired entity was renamed Gate Japan K.K.

The strategic logic is clean. Building a new JFSA-registered entity from scratch would have taken three to five years with uncertain outcomes. Acquiring an existing licensed entity converted a process that takes years into a closing transaction. The licence came with operational continuity, Japanese senior management who had passed the FSA's fit-and-proper test, and AML systems already accepted by the regulator. Gate inherited a market entry instead of building one.

The headline insight is not "buy your way in." It is that some regulatory regimes structurally prefer the acquisition path. The FSA's preferred channel is not a faster greenfield application. It is a transfer of an existing licensed entity to acceptable new ownership.

The Turkey Move: Localise and Wait Through the Regime

Turkey is the inverse of Japan in licensing maturity. The Capital Markets Board (CMB) issued Communiqués III-35/B.1 and III-35/B.2 on 13 March 2025, formally establishing the Crypto Asset Service Provider (CASP) regime. Before that date, Turkey had AML rules under MASAK but no operating licence regime for crypto exchanges. The 2025 communiqués were the first attempt at one.

The CASP regime requires a CMB-issued operating licence for any exchange, wallet provider, or custodian serving Turkish residents. Minimum charter capital is set at 150 million Turkish lira (approximately USD 4.1 million) for exchanges and 500 million lira (USD 13.7 million) for custodians. Licensed operators pay a 2% revenue-based fee annually, with 1% going to the CMB and 1% to TUBITAK. MASAK Circular No. 29, issued in 2025, introduced withdrawal period restrictions, stablecoin limits, and transaction disclosure rules on top of the licensing layer.

The application timeline is the operative regulatory clock. The deadline to submit an operating licence application was 30 June 2025. The deadline to obtain a final certificate of authorisation is 30 June 2026.

Gate's response was to localise the operating entity. Gate operates a dedicated Turkish facing platform through gate.tr, separate from the global Gate.io. There was no existing licensed entity to acquire because the licensing regime itself was new. The path was to register a Turkish entity, capitalise it to the CASP threshold, and submit to the CMB process during the transition window.

This is not the Japan path. There is no shortcut entity to buy. The strategy is to inhabit the licensing regime as it is being built and to receive the licence when the regulator issues it.

The United States Move: Accumulate Thirty-Five State Licences

The United States has the most architecturally fragmented crypto regulatory regime in the world. At the federal level, an exchange registers as a Money Services Business with the Financial Crimes Enforcement Network (FinCEN) under the Bank Secrecy Act. That is the entry-level filing. The real work is at state level. Forty-nine states plus the District of Columbia require a Money Transmitter Licence (MTL). New York operates a specialised BitLicence regime. California operates under the Digital Financial Assets Law. Each state has its own capital, bonding, custody, and AML rules.

Gate's US strategy, executed through Gate US LLC, was to register the federal MSB with FinCEN in 2022 and then accumulate state MTLs one jurisdiction at a time. As of the most recent publications, Gate US holds 35 state-level MTLs and operates across 46 jurisdictions. Notable exclusions remain New York under the BitLicence regime and Hawaii under its specialised licensing regime. The 35-state footprint took approximately three years to assemble.

This path is the opposite of Japan in three dimensions. There was no national entity to acquire because no national equivalent exists. The pace was constrained by 35 separate regulator approvals, not one. And the cost was distributed across years of state-by-state filings, fees, and capital posting.

The compensating advantage is structural. No single regulator can withdraw Gate's entire US footprint. A New York-style enforcement action against one US entity would not unwind the other state licences. The licence portfolio is diversified by construction.

The Europe Move: One Licence, Twenty-Seven Markets

Europe illustrates a fourth pattern. Gate Technology Ltd, a Maltese entity within Gate Group, obtained a MiCA Licence from the Malta Financial Services Authority (MFSA) in October 2025, joining a list of major exchanges, including Coinbase, Kraken, Bitpanda, Bybit, and OKX, that secured the same passporting authorisation. MiCA allows a single licensed EU entity to provide exchange and custody services across all 27 member states, covering 450 million residents. Gate also holds a Maltese Payment Institution licence and operated under Malta's earlier VFA regime dating from 2022.

The Europe path is "one regulator, many markets." It is the dimensional opposite of the United States. One supervisory relationship, twenty-seven national markets, single capital threshold, harmonised conduct rules.

The Architectural Pattern

Four markets, four different operating models. The pattern is not "find the cheapest licence." The pattern is "match the entity structure to the regulator's preferred channel."

The JFSA prefers regulated entities operated by Japanese management. Gate acquired one. The CMB built a new licensing regime from scratch. Gate registered a new entity to receive the new licence. US state regulators require licensed money transmitters. Gate accumulated 35 of them. The MFSA was the first EU regulator to operationalise MiCA at scale. Gate built its EU entity in Malta.

Three observations follow.

First, the cost of compliance scales with the depth of market access. Acquiring Coin Master cost an acquisition price in the millions for one country. The US state-by-state path involved 35 separate licensing processes, each with its own legal fees and capital requirements, probably running into tens of millions over three years. The MiCA application required a Maltese subsidiary, MFSA-aligned governance, and ongoing supervisory engagement. The architecture is not optimising for cost. It is optimising for licence quality.

Second, licence quality determines the depth of services Gate can offer. A licensed Japanese entity can serve Japanese institutional clients that a global Gate.io account cannot. A MiCA-licensed entity can be on a European bank's counterparty list. A state-licensed US entity can hold customer funds under state custody rules. The differentiating service tier on top of any crypto exchange is access to regulated institutional flows. That tier is gated by licence quality, not by trading technology.

Third, the compliance footprint is a competitive moat that no marketing campaign can replicate. A competitor entering Japan today faces the same JFSA process Gate would have faced in 2024. There is no shortcut. There is no growth hack. There is no token launch that makes the regulator move faster. A regulatory footprint is an accumulated asset, and accumulated assets cannot be replicated by faster competitors.

Why This Echoes the Malaysian Property Stack

I have written before about the Malaysian property regulation stack: the Valuers, Appraisers and Estate Agents Act 1981 (Act 118), the LPPEH enforcement layer, the JPPH data layer, and the BNM payment layer. The argument there was that PropTech companies that survive treat regulation as the operating system, not as the ceiling.

The Gate.io case is the international generalisation of the same principle. Four markets, four regulatory stacks, four entity structures. The corporate parent functions as the unifying layer above them, but each subsidiary is structurally native to its market.

The principle scales across two axes that look unrelated. One axis is local and deep: a single market with multiple regulatory layers stacked on top of each other, which is the Malaysian case. The other axis is global and broad: a single firm operating across four markets, each with its own stack, which is the Gate case. The architectural insight holds in both directions. Read the regulatory stack first. Engineer the product entity to inhabit that stack. Treat the licence footprint as the long-term accumulated asset that defines what services you can offer.

Three Takeaways for Founders

If you are building a fintech, paytech, or any regulated market product, three things from this case are worth holding onto.

-

Read the regulator's preferred channel before designing your entry path. The JFSA prefers acquisition. The CMB prefers a new locally-incorporated entity. The US prefers state-by-state accumulation. The MFSA prefers a Maltese subsidiary. Trying to push a single entry model across all of them is the mistake.

-

Accept that one global entity cannot serve all markets. Gate has at least five operating entities: Gate.io global, Gate Japan K.K., Gate US LLC, Gate Technology Ltd, and gate.tr. The corporate parent is not the operating entity. The operating entity is jurisdiction-specific.

-

Treat compliance footprint as an accumulated asset, not a recurring cost. The 35-state US footprint is worth more than its assembly cost. The Japanese FSA registration No. 00018 cannot be replicated by a faster competitor at any price. The MiCA passport is worth more in 2026 than it was when MFSA issued it.

Regulation, read correctly, is not the friction that slows a product down. It is the architectural substrate that decides which products are allowed to exist at scale.

KG previously worked at Gate.io and currently serves as General Manager of PEPS Ventures Berhad, where he oversees product and regulatory strategy for ValuationXchange, PaymentXchange, and Valuer Copilot.

Strategy and technology are the same decision. Over 15 years in fintech (CTOS, D&B), prop-tech (PropertyGuru DataSense), and digital startups, I have built frameworks that help founders and executives make both moves at once. Based in Kuala Lumpur.

Working on a 0→1 product?

I help founders and operators go from idea to validated product. Let's talk about yours.

Get in touch →