Services Are the New Software: The Autopilot Wedge for SEA Fintech and Regtech

The Shift Inside Twelve Months

In 2025, the fastest-growing AI companies were copilots. They sold tools to professionals: a junior accountant got a smarter spreadsheet, a paralegal got a faster reviewer, a developer got an autocomplete that finally understood the codebase.

In 2026, the same companies are racing to become something else. They are trying to sell the work, not the tool.

The framing is from Julien Bek at Sequoia, in a piece titled Services: The New Software. His thesis is simple. For every dollar spent on software, six are spent on services. The next trillion-dollar company will not be a better tool. It will be a software company that has positioned itself inside the services budget.

That sentence reframes the entire AI buildout. And it lands particularly hard for anyone running a fintech or regtech practice in Southeast Asia.

What the Deployment Data Actually Says

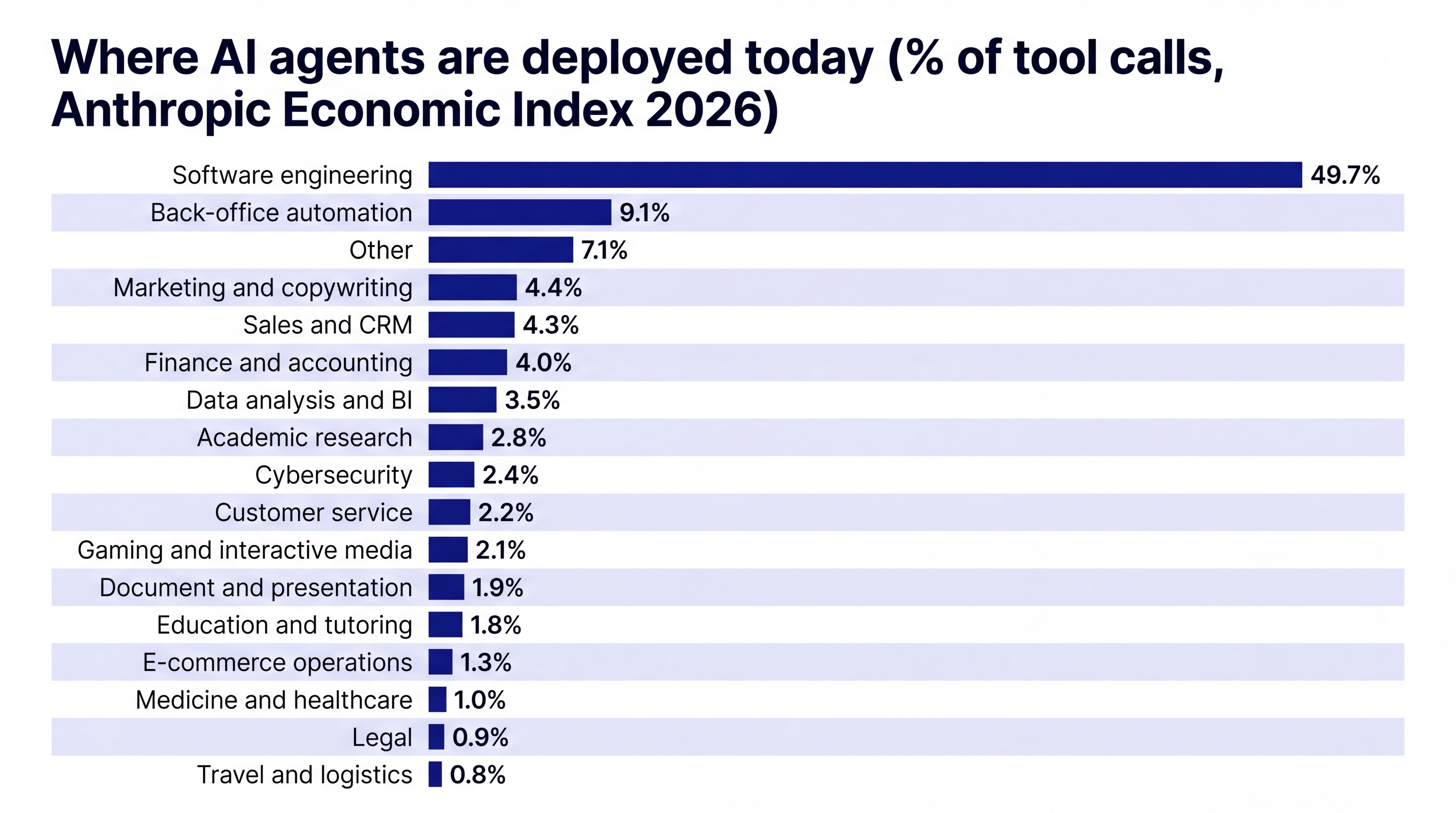

The chart above tracks where AI agents are deployed today, measured by share of tool calls across Anthropic's API traffic. Software engineering dominates at 49.7 percent. Everything else fights for the remaining half.

The instinct is to read this as a coding story. It is not. Software engineering is the leading indicator, not the destination. The reason coders adopted first is that their work is primarily intelligence: rule-bound, verifiable, decomposable. Once the model gets good at intelligence, every other field where intelligence is the binding constraint follows.

Look at the next tier. Back-office automation. Marketing. Sales. Finance and accounting. Data analysis. These are not coding categories. They are services categories where the work product is a document, a report, a reconciliation, a follow-up. And the share is growing fastest there, not in engineering, which has nearly saturated.

The chart is showing the moment before the rest of the economy moves.

Copilots Sell Tools, Autopilots Sell Outcomes

Bek's distinction is worth holding cleanly.

A copilot sells a tool to a professional. The professional remains in the chair. The professional remains responsible. The tool makes them faster. The customer is still buying the seat.

An autopilot sells completed work to the end-user. There is no professional in the middle. The customer is buying the deliverable: the filed return, the cleared claim, the closed ledger.

"If you sell the tool, you are in a race against the model. But if you sell the work, every improvement makes your service faster."

The economics of these two positions are not adjacent. They are different markets. The copilot competes inside the software line item. The autopilot competes inside the services line item, which in most enterprises is many multiples larger. A five times intelligence improvement is a feature upgrade for a copilot. For an autopilot, it is gross margin expansion.

There is a second-order effect worth naming. Copilots that get too good face an innovator's dilemma. The better the tool, the less work the customer has left to do. The customer keeps less of the budget. Pure-play autopilots have no such conflict: every model improvement makes them faster, cheaper, and more profitable simultaneously.

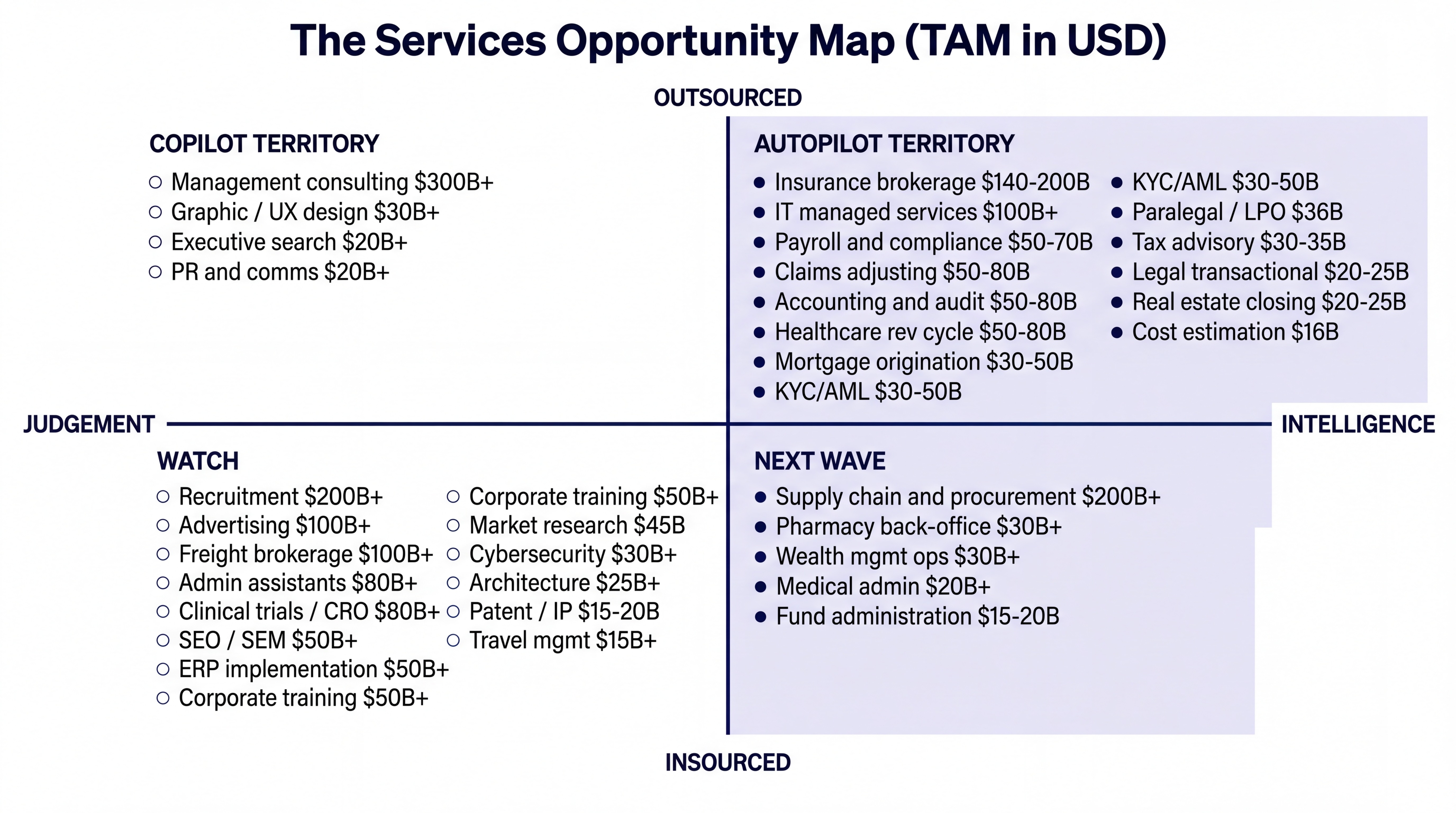

The Opportunity Map

The chart maps services categories on two axes. Horizontal: how much of the work is intelligence versus judgement. Vertical: how much of the work is outsourced versus insourced.

The top-right quadrant is the autopilot territory. The categories there share three properties: the work is intelligence-heavy, an external vendor model already exists, and the buyer already pays for outcomes rather than headcount. Insurance brokerage at 140 to 200 billion USD. IT managed services at 100 billion plus. Payroll and compliance at 50 to 70 billion. Claims adjusting at 50 to 80 billion. Accounting and audit at 50 to 80 billion of US outsourced spend. Healthcare revenue cycle at 50 to 80 billion. KYC and AML at 30 to 50 billion. Paralegal at 36 billion. Tax advisory at 30 to 35 billion. Legal transactional at 20 to 25 billion. Cost estimation at 16 billion.

The top-left is copilot territory. Management consulting at 300 billion plus, graphic and UX design at 30 billion, executive search, PR. The work is too judgement-heavy to autopilot cleanly today. Selling the tool is still the right business.

The bottom-right is the next wave. Supply chain and procurement at 200 billion plus. Pharmacy back-office. Wealth management operations. Medical admin. Fund administration. These are insourced today, but the bridge from copilot to autopilot is already being walked.

The bottom-left is the watch quadrant. Recruitment, advertising, freight brokerage, admin assistants, clinical trials, SEO and SEM, ERP implementation. These categories will be reshaped, but the path is not clean. Human relationships, distribution power, and regulatory drag complicate the takeover.

The Read for Southeast Asia

The map is American. The TAMs are American. The interesting question is which slices of it the SEA market can serve, defend, and own.

Five verticals stand out.

KYC and AML. Every bank, e-money issuer, capital markets intermediary, and crypto exchange in the region is buying ongoing transaction monitoring and customer due diligence as a service. The work product is a clear-or-escalate decision on a counterparty or a transaction. It is pure intelligence. It is already outsourced to a mix of in-region vendors and offshore back-offices. Regulators are open to AI-driven KYC, especially under BNM's e-KYC policy framework and MAS's equivalent. A vendor swap from a manual outsourcer to an autopilot is a procurement decision, not a reorg.

Claims handling. Particularly motor and health. The work is structured: ingest a first notice of loss, triage, request documents, compute the settlement, pay or deny. The TPAs that handle Malaysian general insurance run on payrolls of adjusters and call centres. An autopilot that takes the first notice and returns a decision can collapse two days of work into ten minutes. The insurer does not buy a tool. The insurer buys cycle time.

Accounting and audit. Malaysia has the same CPA shortage as the US, scaled down. Mid-tier firms cannot recruit fast enough to grow. The work most senior managers do today is review work: reconciliations, schedules, draft notes. An autopilot that delivers a reviewed set of schedules ready for partner sign-off is not selling software. It is selling associate hours. The buyer for that is every firm with a partner-to-staff ratio that has stopped working.

Mortgage origination. Malaysian banks have the underwriting workflow split across internal credit officers and external panel valuers, panel lawyers, and panel insurers. The choreography is the bottleneck, not the credit decision. An autopilot that runs the choreography end-to-end and surfaces a packaged file for a one-touch decision compresses turnaround from weeks to days. The bank does not procure a copilot. The bank procures a faster origination engine.

Real estate closing. Conveyancing in Malaysia is paperwork-dense, deadline-driven, and largely standardised. The same panel lawyer handles a hundred sale and purchase agreements a year, each one ninety percent identical. The autopilot here is a service that produces a complete, signable closing package against a deal envelope. The buyer is the agent or the bank, not the lawyer.

Why the Wedge Works in SEA

Three reasons the autopilot thesis travels well to this region.

First, vendor swap is the default purchasing motion. Malaysian financial institutions, hospitals, and corporates are already comfortable contracting out structured work to external firms. They do not need to be sold on the idea that someone outside the building does the job. They only need to be sold on the idea that the new vendor is faster, cheaper, and equally accountable. That is a one-axis sale, not a transformation project.

Second, the regulators are working with the grain. BNM's regulatory sandbox, the Securities Commission's digital innovation framework, and the cross-border data-sharing arrangements with Singapore are all pointed at the same outcome: encourage automation of compliance work, do not entrench the manual incumbents. The licensing surface for many of these verticals is smaller than in the US, which lowers the cost of entry for autopilot-native firms.

Third, data fragmentation is a feature, not a bug. The Malaysian property market, the local credit bureau coverage, the local insurance loss tables, and the local case law are all distinct datasets that a global player will not casually replicate. A local autopilot that compounds proprietary data on its own customer base has a moat that a US or India operator cannot trivially cross. The data is small, but it is small here. That works in the defender's favour.

The Honest Risk for Incumbent Practices

If you run an accounting practice, a tax shop, a panel law firm, or a TPA today, the map above is not flattering.

You are the customer being replaced. The buyer you are selling to is the same buyer the autopilot will sell to next year. The autopilot will charge less per file, deliver faster, and improve every quarter. Your fixed cost base of partners and associates will not.

The decision is binary. Either you bet the practice on becoming the autopilot for your slice of work, which means changing the business model, the hiring profile, and the pricing structure inside twelve to eighteen months. Or you accept margin compression and shrink gracefully, which is a viable strategy if your goal is to harvest the existing book and exit.

The middle path of adopting copilots while keeping the billing-by-hour model is the trap. It improves throughput but does not change the unit economics. When the customer figures out that the work is now ninety percent machine, the customer renegotiates the rate. The copilot saves cost for the practice. The autopilot captures revenue for someone else.

Three Moves to Make This Year

If you are choosing the autopilot path, three moves matter.

Pick one workflow you can productise end-to-end. Not a feature. A complete service line where the deliverable is unambiguous and the input is structured. Ongoing KYC monitoring for one segment. Motor claims under a single coverage type. Statutory accounts for SMEs under a revenue band. The narrower the better. The autopilot wins by going deep on a sliver, not wide on a category.

Charge by the outcome, not the hour. Per file, per case, per closing. The moment the price stops scaling with headcount, the business model is ready to absorb AI margin. Until then, every productivity gain leaks back to the customer through fewer billable hours.

Build a data moat from the work you already do. Every file your team processes is a labelled training example. The autopilot that wins a vertical in five years will be the one that has been collecting clean, structured outcome data from year one. Start the schema before the model needs it.

The Quiet Conclusion

The trillion-dollar SEA company that emerges from this cycle will not look like Grab or Stripe. It will look like a back-office tax shop, a claims adjuster, or a panel law firm, except no client ever meets a human. The work product arrives on time, costs a fraction of the manual equivalent, and improves silently every quarter as the model that runs underneath gets better.

Sequoia's framing is that services are the new software. The translation for SEA is sharper than that. Services are the only software worth writing. The tool budget is small and shrinking. The work budget is large and migrating to whoever shows up with an autopilot first.

The window opens this year. It does not stay open long.

Strategy and technology are the same decision. Over 15 years in fintech (CTOS, D&B), prop-tech (PropertyGuru DataSense), and digital startups, I have built frameworks that help founders and executives make both moves at once. Based in Kuala Lumpur.

Working on a 0→1 product?

I help founders and operators go from idea to validated product. Let's talk about yours.

Get in touch →