AI and Crypto: The Infrastructure Nobody Saw Coming

The entire cryptocurrency industry has been chasing the wrong target audience.

For 15 years, founders have tried to convince humans that blockchain is a better way to send money, store value, or invest. It has never worked. The technology is genuinely worse for humans at almost every measure that matters: speed, user experience, fees, reversibility, and recourse.

But there is a different user that has been waiting in the wings. One that does not sleep. One that does not care about human-friendly interfaces. One that needs trustless settlement, always-on operation, and programmable transaction logic.

Autonomous AI agents.

Here is the core tension: we have spent 15 years trying to convince humans to use blockchain. The entire time, the real users were never humans. They were the autonomous agents we were busy building in parallel. Crypto was not designed for us. It was designed for the machines we are now building to work 24/7 with each other.

Why Agents Need What Humans Don't

To understand why crypto infrastructure is perfect for AI agents, start with why it is terrible for humans.

A human wants to send money to a colleague. A wire transfer works. Fast enough, cost is built into the bank relationship, and if something goes wrong, a customer service team investigates. Blockchain requires self-custody of keys, a network fee, a 10 to 30-minute wait for settlement, and zero recourse on mistakes. Blockchain loses on every dimension for this use case.

Now consider an AI agent conducting invoicing for a software company. The agent needs to:

- Verify that the customer is real (blockchain identity verification)

- Execute the transaction without human approval (smart contracts)

- Settle immediately, not in three days (on-chain settlement)

- Create an immutable record for audit (blockchain ledger)

- Coordinate with other agents (trustless verification)

- Work 24/7 (no bank operating hours)

For the agent, blockchain wins on every dimension. A traditional bank is slow, requires human authorization, has limited operating hours, and creates centralized records that can be altered. Blockchain is fast, trustless, always-on, and immutable.

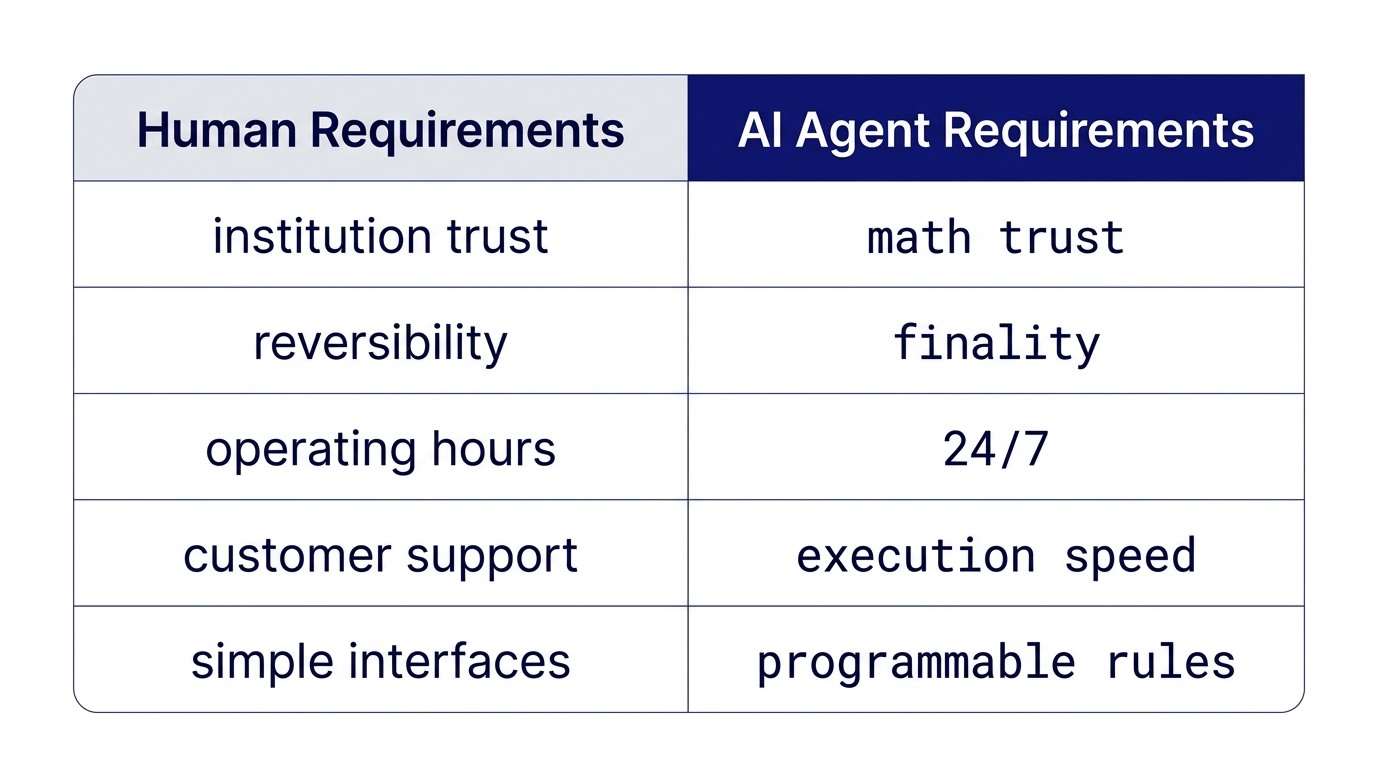

The disconnect is fundamental. Humans and agents have opposite requirements. Humans want an institution they can trust. Agents want to trust math. Humans want customer support. Agents want execution speed. Humans want reversibility. Agents want finality.

For 15 years, crypto was built around human requirements, which is why it failed at consumer adoption. Now it is being rebuilt around agent requirements, which is why it will succeed at scale.

Know-Your-Agent: The Credential System for Autonomous Transactions

The first piece of this infrastructure is already emerging: Know-Your-Agent (KYA) credentials. These are not traditional legal documents or compliance frameworks. They are technical contracts stored on-chain that define an AI agent's identity and transaction authority.

Here is how it works.

An AI agent is deployed by a company. The agent has a wallet address as its on-chain identity. The deploying company signs a KYA credential that specifies:

- Which agent this credential belongs to (cryptographic identifier)

- What transaction types it is authorized to execute

- What limits apply (maximum transaction size, hourly volume caps)

- What audit trail requirements are embedded (regulatory compliance rules)

- What conditions invalidate the credential

That credential is stored on-chain. Other agents and systems can read it. They can verify that a transaction request is coming from a legitimate agent operating within its defined scope. No centralized approval point. No human in the loop. Just cryptographic verification.

The credential is programmable. You can layer conditions: agent can transact only during business hours, agent must flag transactions over a certain threshold for human review, agent cannot transact with other agents that lack a valid KYA credential. The rules are code.

For regulated industries in Southeast Asia, this solves a critical problem: how do you allow AI agents to operate autonomously while maintaining regulatory control and audit trails? KYA credentials let you define operating parameters transparently, enforce them cryptographically, and maintain a permanent record of every decision the agent made and why.

The 24/7 Settlement Reality

Here is where the economics get real.

A traditional bank operates Monday through Friday, 8 AM to 5 PM. Invoice settlement takes three days. A software company invoices its customers on Tuesday. The bank processes them Thursday. Settlement happens Friday. The company operates in perpetual settlement lag.

An AI agent using blockchain operates 24/7. Invoice arrives at 2 AM Tuesday. The agent verifies it, executes the transaction, and settlement is final at 2:15 AM. The company sees cash immediately. No settlement lag. No operating hour constraints. No waiting for the bank to wake up.

For a business processing high volumes of B2B invoices, this is not a nice-to-have. It is a fundamental shift in working capital management. If your invoices settle in three days, you need operating capital to cover the gap. If they settle in 15 minutes, you need a fraction of that capital. The leverage is significant.

Multiply this across thousands of agents, billions of transactions per year, and you see why AI agents holding 30 to 80% of crypto market value by 2030 is not a speculative claim. It is a working capital infrastructure story.

The Management Accounting Shift

Here is where my lens as a chartered management accountant (ACMA, CGMA) becomes relevant.

If AI agents are transacting autonomously on-chain, who reconciles? Not in the sense of human review, but in the literal sense: how do you record this activity in the general ledger? Who defines the chart of accounts for an agent's financial activity?

In traditional accounting, a human submits an invoice, a human approves it, a human records it, a human verifies it. Four decision points, four human controls. With agent-to-agent transactions, the agent receives the invoice, verifies authenticity, matches to a purchase order, authorizes payment, and records the transaction. All in seconds. All auditable. All permanent.

Consider a concrete scenario in property finance:

A property developer needs a valuation from multiple firms. Instead of hiring each firm separately and waiting weeks for reports, the developer deploys a smart contract specifying: "I will pay 25,000 MYR for a property valuation from any agent with valid KYA credentials from the relevant professional body. Agent executes valuation. If I approve, payment settlement is automatic."

The agent receives the request, verifies the developer's credentials, accesses property databases, executes the valuation, and submits the report. The developer approves in minutes. Payment settles on-chain in seconds. The transaction records in the developer's general ledger as "Property Valuation: PV-2026-03-23" with full audit trail. The valuation firm records "Service Revenue: 25,000 MYR" with full details. Both parties have the same permanent record. No reconciliation required.

The accounting control structure changes. Instead of "Verify, Approve, Record, Audit," it becomes "Define Rules, Execute Autonomously, Record Permanently." The compliance problem shifts from human judgment to code review and governance.

For management accountants and operations leaders, the concrete questions to work through now:

- How do you audit an AI agent's financial activity when settlement is instant and permanent?

- What does "internal controls" look like when code is executing transactions autonomously?

- How do you build a chart of accounts that makes sense for agent-initiated transactions?

- What regulatory frameworks do you need to operate agents in Malaysia, Singapore, and offshore simultaneously?

- How do you calculate working capital and cash forecasting when settlement is real-time?

These are not hypothetical questions. They will show up in audits starting in 2027.

This connects to the broader 0→1 pattern I write about in Brief-then-Fire: the teams building infrastructure for autonomous agent operations today are not working on future problems. They are building the accounting and compliance layer that regulated industries will require within 18 months.

The Longer View

Crypto evangelists talked for years about "disrupting finance." They were always too early and wrong about the mechanism. They thought humans would adopt it. The actual mechanism is simpler and more profound: humans are building autonomous agents that will operate 24/7 in B2B environments. Those agents need infrastructure that is always-on, trustless, and programmable. Traditional finance cannot provide it. Blockchain is purpose-built for it.

The 2030 scenario is not that consumers are using Bitcoin. It is that companies' autonomous agents are holding substantial shares of crypto market value and transacting with other agents around the world with zero human friction, permanent audit trails, and instant settlement.

This shift is already underway. Foundation models are improving. Agent frameworks are shipping. B2B software is moving from "humans using software" to "software using software." The demand for trustless, always-on, programmable transaction rails will grow exponentially.

Crypto is not waiting for mainstream adoption. It is waiting for its actual users. Those users are not in the newsletter you are reading. They are in the data centers and cloud environments where autonomous agents are about to start transacting.

The infrastructure was built. The users are coming. The timing is about right.

Strategy and technology are the same decision. Over 15 years in fintech (CTOS, D&B), prop-tech (PropertyGuru DataSense), and digital startups, I have built frameworks that help founders and executives make both moves at once. Based in Kuala Lumpur.

Working on a 0→1 product?

I help founders and operators go from idea to validated product. Let's talk about yours.

Get in touch →