Computer Vision in Property Valuation: Precision at Scale

An Automated Valuation Model is a skeleton key. It works brilliantly for what it was designed to do: take a property address, cross-reference comparable sales data, apply statistical adjustments, and produce a defensible estimate of value.

It is blind to condition.

A 1,200 square foot apartment, sold twelve months ago for RM 420,000, is the model's comparable. The model knows the address, the price, the timestamp. It treats the information symmetrically: this unit is similar to the subject property, so apply a 3% premium for location and 1.2% discount for time adjustment.

But the model does not know that the comparable's kitchen was last renovated in 1998. It does not see the water stain on the ceiling or the threadbare carpet or the evidence of deferred maintenance. It cannot assess whether the unit was owner-occupied (and therefore maintained) or rented-out (and therefore used hard).

This is where the tension surfaces: property valuation demands precision. The market demands speed. These have always been in tension because precision requires site visits, and site visits take time. Computer vision applied to listing photos dissolves this. You get condition-adjusted precision at database query speed.

In Malaysian property markets, the gap is even wider. NAPIC data is rich in price and location. JPPH records capture use type and legal status, but condition data is almost entirely absent. Valuers fill this gap through site visits, photographs, and subjective assessment. This is slow. It is difficult to replicate. It is hard to audit.

Computer vision sees in a different way.

What Computer Vision Actually Sees

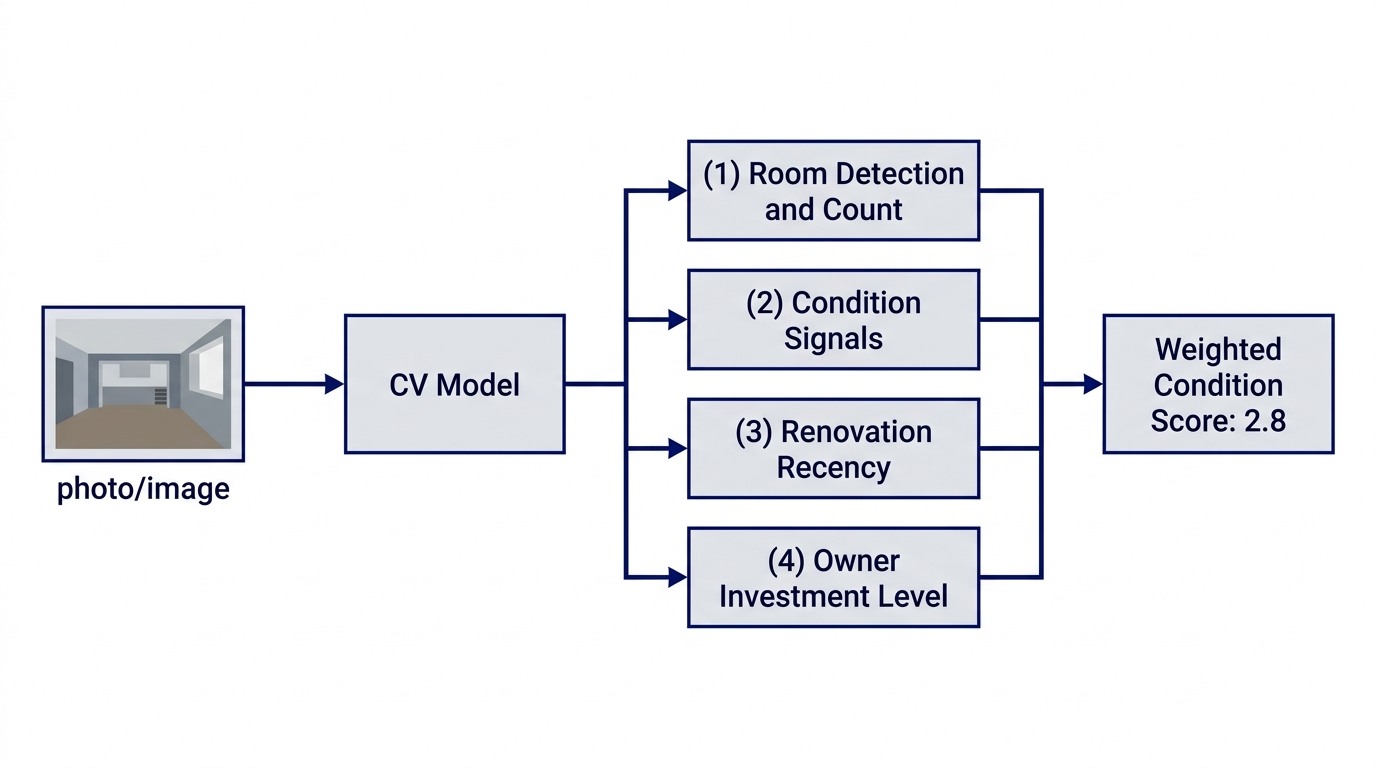

Computer vision applied to property photos is not magic. It is pattern recognition applied systematically to visual information.

When you feed a property listing's photographs into a trained computer vision model, the system does several things in parallel.

Room detection and classification. The model identifies discrete spaces: living room, kitchen, master bedroom, secondary bedrooms, bathrooms, dining area, storage. It counts them. It estimates dimensions and proportions. This alone is more reliable than relying on a listing agent's description, which is often inflated or vague.

Condition signal detection. The model looks for visual markers of condition: paint condition (glossy or flat, faded or fresh), flooring wear (scuffing, staining, material apparent), wall and ceiling condition (cracks, stains, moisture evidence), fixture age (based on design language and finish quality). These are not subjective judgments. These are features the model has been trained to detect and score.

Renovation recency and quality assessment. By analyzing fixture design language, material finishes, and overall aesthetic coherence, the model can estimate when major renovations occurred and whether they were professional or DIY. A kitchen with mismatched cabinet finishes, amateur tiling, and incomplete caulking scores differently from one with consistent designer finishes and professional installation.

Owner investment level inference. Furniture choice, decor consistency, and overall maintenance signals allow the model to infer owner investment level. A unit with carefully curated furniture and fresh paint indicates active owner engagement. A unit with functional-only furniture and visible neglect indicates passive or cost-constrained ownership.

None of this is definitive, but none of it is subjective either. Each signal is scorable. Each score compounds into a comparable condition rating.

Here is the practical output: instead of categorizing comparables as "good/average/poor" (vague, difficult to defend), you rate them on a 1-5 scale per room type, then weight them into an overall property condition score.

A kitchen scores 2 (dated finishes, 1998 era). A master bath scores 1 (original fixtures, water stains). Bedrooms score 3 (worn carpet, clean walls). Living spaces score 3 to 4 (maintained, no recent updates). Overall weighted condition score: 2.8.

Now you have a comparable with a condition score of 2.8. You have another comparable with a condition score of 4.2. The first is less similar to a subject property with condition score 3.8 than the second. Your comparable selection logic improves. Your adjustments become more precise.

And this took minutes, not days.

The Malaysian Market Context: Where the Gap Is Widest

Condition assessment matters everywhere in property valuation, but it matters more in Malaysia for a specific reason: our comparables data is thin, and our condition information is almost non-existent in formal records.

NAPIC tells you price, area, land use, legal status. JPPH tells you building age and zoning. Banks have transaction history and loan-to-value ratios, but none of this tells you condition.

In a transparent market like Singapore or Australia, condition data is embedded in professional standards. Every valuation includes a condition assessment. Comparable sales listings include photographs and condition notes. The comparable pool is rich with information.

Malaysia's comparable pool is information-poor. Valuers fill the gap through site visits and photographic evidence. This is defensible, but it is labor-intensive.

Computer vision inverts this problem. It makes the comparable pool information-rich in the dimension that currently matters most: condition.

Think about what this means for a bank managing a mortgage book of 15,000 units across multiple territories and building types.

Traditional valuation approach: physical site visits, manual condition assessment by a qualified valuer, comparable selection from regional data, report drafting and quality review, delivery. Timeline: 4 weeks for an effective portfolio assessment. Cost: significant.

With a computer vision pipeline: listing photos (or field inspection photos) are uploaded, condition scoring runs overnight via cloud-based model, comparable selection logic applies condition-scored comparables, report templates auto-populate with condition data and comparable explanations, valuer reviews and approves and delivers. Timeline: 2 weeks. Cost: significantly reduced. Precision: higher than manual assessment.

The Workflow Integration: From Inspection to Report

Let me walk through the actual workflow, because this is where the speed gain becomes concrete.

A field valuer is assigned a portfolio of 50 properties for condition assessment and valuation.

Today, the workflow:

- Visit each property (2 to 3 hours per property)

- Take notes and photographs

- Return to office

- Write up condition assessment (1 to 2 hours per property)

- Select comparables manually

- Apply adjustments

- Draft valuation report

- Quality review and client delivery

Total time per property: 6 to 8 hours. Portfolio of 50 properties: 300 to 400 hours. That is 8 to 10 weeks.

With computer vision integration:

- Visit each property (same as above)

- Take standardized photographs (same camera angles, same lighting conditions)

- Upload to cloud during or immediately after inspection

- Return to office

- Condition scoring completes overnight via CV model

- Comparable selection logic auto-filters by condition score, applies structured adjustments

- Report template auto-populates with condition data, comparable rationale, valuation conclusion

- Valuer reviews and approves (validates, does not rewrite)

- Client delivery

Total time per property: 4 to 5 hours. Portfolio of 50 properties: 200 to 250 hours. That is 5 to 6 weeks. Quality: higher (systematic condition scoring, transparent and auditable comparable selection).

The field valuer's time becomes allocation-efficient. Senior review time is preserved for judgment-intensive decisions (comparable selection, adjustment reasonableness, conclusion defensibility). Junior or technical staff can execute the CV workflow without requiring senior supervision on every step.

The Precision Angle: Condition-Adjusted Comparable Selection

Here is where computer vision has its biggest impact: improving the quality of comparable selection.

A traditional comparable selection process:

- Identify properties that sold recently in a similar location

- Filter by size (within 10 to 15%)

- Filter by age (within 5 to 10 years)

- Select 3 to 5 best matches

- Note condition differences and apply qualitative adjustments

The problem: step 5 is where precision is lost. How much should you adjust for condition? How do you defend that adjustment to a client or a regulator?

If you have condition scores from computer vision, the selection logic tightens:

- Identify properties that sold recently in a similar location

- Filter by size (within 10 to 15%)

- Filter by age (within 5 to 10 years)

- Filter by condition score (within 0.5 points on a 1-5 scale)

- Select 3 to 5 best matches

- Note remaining differences and apply adjustments to non-condition factors

Condition is no longer a qualitative adjustment. It is a selection criterion. This changes the comparable pool and the adjustment profile entirely.

A typical valuation might have seen a 5 to 8% condition adjustment applied to one or more of a three-property comparable set. With condition-filtered selection, you might see a 1 to 2% adjustment (because condition is already close-matched) applied to fewer comparables.

This is not just faster. It is more defensible. Regulators (LPPEH, JPPH, courts) can see exactly how condition was measured, how it was compared, and how it was adjusted. The process is transparent.

The same principle applies here as in the Hybrid SQL+Vector Search architecture: the goal is a system that is both precise and defensible. Condition scoring via CV is the quality input that makes comparable selection tighter at both layers.

Portfolio-Level Capability: The Bank Use Case

Think at scale.

A bank holds a mortgage portfolio of 10,000 properties. It wants to understand collateral risk across the book. It wants to answer:

- How many units are in poor condition (condition score below 2)?

- What is the average condition score by district, by building age, by property type?

- Which units might need condition-based risk weightings in loan provisioning?

- Which units should trigger enhanced monitoring?

Traditional approach: sample audit. The bank assesses a statistically valid sample (200 to 300 properties), then extrapolates. This takes weeks and only covers a sample.

Computer vision approach: condition-score the entire book. Listing photos (sourced from past bank valuations, property portals, or new field inspections) feed the CV model. Overnight, 10,000 properties have condition scores. The bank now has full-book visibility into condition distribution, can identify outliers, can stress-test collateral value under condition degradation scenarios, and can allocate monitoring resources to highest-risk cohorts.

In Malaysia, where collateral quality data has historically been a blind spot, this is a structural advantage. A lender who can quantify collateral condition at portfolio level can price risk more accurately, identify problem cohorts earlier, and manage loss severity more effectively.

This is the kind of product capability I describe in How I Run 0→1 Product Sprints: find the workflow where AI closes a gap that was previously closed by manual labor, build the minimum viable pipeline, measure the accuracy lift, scale from there.

The Regulatory Reality: Decision Support, Not Replacement

Here is where I need to be clear about limits.

Computer vision does not replace human valuation judgment. IVSC standards, LPPEH guidelines, and common law expect human judgment in valuation. A valuer must be a qualified professional who can explain and defend conclusions.

What CV does is remove the mechanical labor from valuation and provide decision-quality inputs for the judgment layer.

A qualified valuer using CV-derived condition scores and CV-assisted comparable selection can produce an opinion of value that is more defensible (because the inputs are systematic and auditable), faster (because mechanical work is automated), and more precise (because condition is quantified instead of estimated).

The professional still owns the conclusion. The regulatory standard is still met, but the path to that conclusion is more efficient and more auditable.

This is the same framework that applies to Automated Valuation Models. AVMs are not valuations. They are decision support. A valuer using an AVM as one input to their professional judgment is operating within standards. A system that replaces professional judgment is not.

Computer vision sits at the same level as an AVM: a capability that a qualified professional can employ to improve their work, not a replacement for that work.

Precision Meets Speed

We started with a tension: precision demands time. Speed compromises accuracy.

Computer vision dissolves this.

You get condition-adjusted precision (fine-grained, auditable, comparable-specific) at the speed of a database query. A field valuer can assess 200 properties in a week with condition-scored reports ready within 48 hours of inspection. A bank can condition-score a mortgage book of 10,000 units in a single processing cycle.

The margin structure changes. The time-to-revenue cycle compresses. The decision quality improves.

For property valuers in Malaysia, this is a capability that separates practitioners from commodities. The valuer who has built a CV-integrated workflow can serve clients at speed and precision that competitors without this capability cannot match. The bank with portfolio-level condition scoring can price and manage collateral risk with precision that competitors cannot.

The question is not whether this is coming. It is here. The question is whether your firm is building the capability or waiting to acquire it.

Start with one use case. One property type. One comparable selection challenge. Build the CV pipeline. Measure the lift in speed and precision. Scale from there.

The market has already moved. The question is where you are standing.

Strategy and technology are the same decision. Over 15 years in fintech (CTOS, D&B), prop-tech (PropertyGuru DataSense), and digital startups, I have built frameworks that help founders and executives make both moves at once. Based in Kuala Lumpur.

Working on a 0→1 product?

I help founders and operators go from idea to validated product. Let's talk about yours.

Get in touch →