Satellite AI Foundation Models: The Democratization Trap

Meta's earth observation team announced a 1-meter resolution global tree-height map using DINOv2, a Vision Transformer foundation model trained on 1.2 billion unlabeled images. IBM released TerraTorch, a framework for fine-tuning geospatial foundation models on custom datasets. A consortium of researchers published ChatEarthNet, combining Sentinel-2 satellite imagery with natural language models to automate analysis workflows. All within the past three months.

The industry consensus is euphoric. Geospatial intelligence is democratizing. The barrier to entry is collapsing.

Which is true. Which is also the exact moment when specialized firms should start sweating.

Here is the named tension: we celebrate that foundation models democratize geospatial intelligence. Simultaneously, they remove the competitive moat everyone assumed they had. Democratization that lifts everyone also drowns anyone standing still.

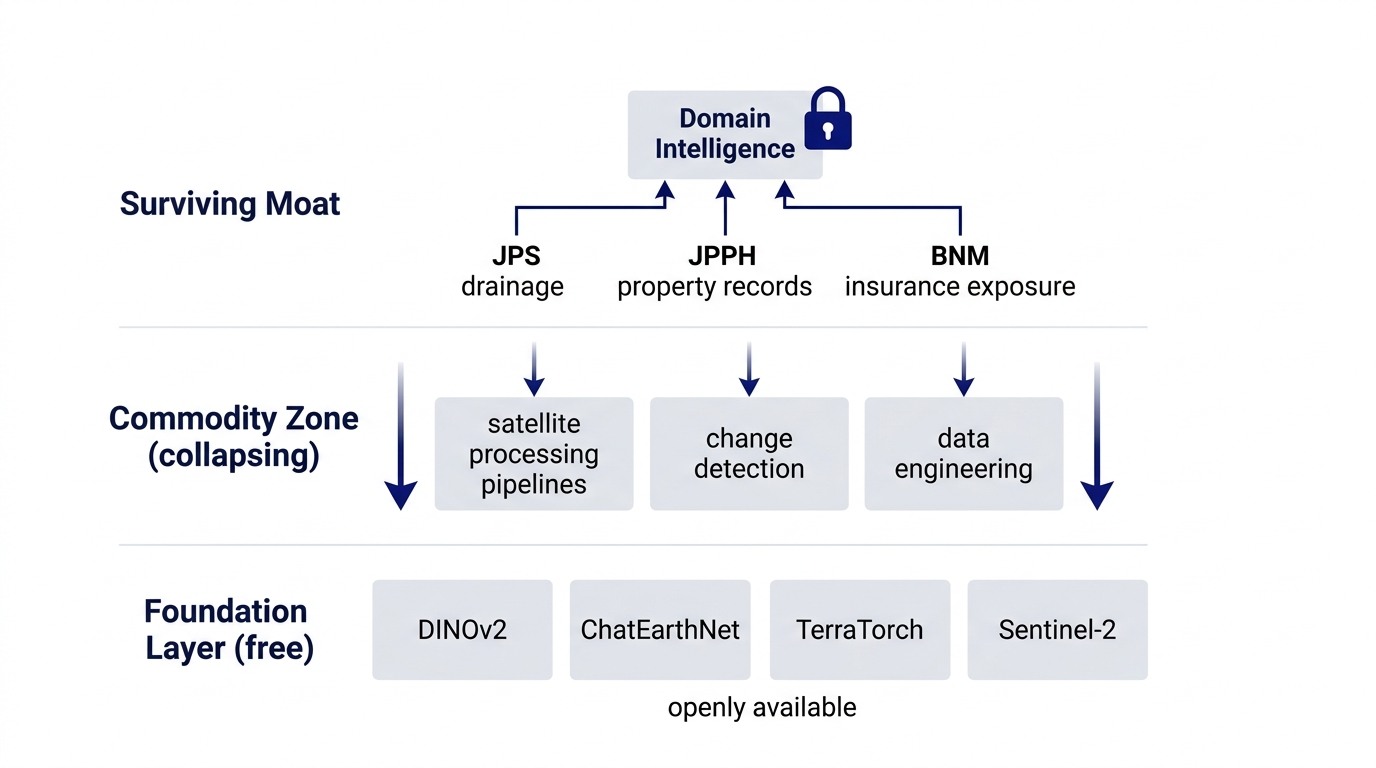

The Commodity Layer Vanishes

For the last decade, geospatial intelligence meant satellite data processing. You needed specialists in radiometric correction, orthorectification, change detection, and multi-temporal analysis. You needed expensive infrastructure to store and process terabytes of imagery. You needed proprietary algorithms to extract meaning from the noise.

DINOv2 changed that. A Vision Transformer trained on 1.2 billion unlabeled images learned to recognize texture, structure, and context so deeply that it extracts useful features from satellite imagery without ever being trained on satellite data. You feed it Sentinel-2, Landsat, or high-resolution commercial imagery. The model has already learned what trees look like, what water looks like, what urban development looks like. It does not care that the input is satellite data.

For geospatial firms, this is the moment the specialized moat evaporates.

Here is what happens next: a team of six people, working from a garage or a university, builds a flood-risk model in three weeks using Meta's tree-height data, DINOv2 features, and a standard classifier. That team costs you one senior hire. Their cost structure is an API call and a GPU instance. They do not need your ten-person data engineering team. They do not need your two years of accumulated processing pipelines. They need a research paper and a GitHub repository.

IBM TerraTorch accelerates this further. It simplifies fine-tuning geospatial foundation models on proprietary datasets. The dream of specialized geospatial modeling becomes a technical implementation detail, not a competitive advantage. Anyone with a GPU and labeled data can now fine-tune a foundation model in weeks instead of building a bespoke pipeline in months.

ChatEarthNet is the last piece. It combines Sentinel-2 imagery (freely available from the European Commission) with NLP models to automate analysis workflows. "Assess this area for flood risk." "Categorize crop health across this region." "Detect urban expansion." The model takes an English instruction and satellite imagery, then produces an analysis. The time-to-insight compresses from months to days.

The compressed timeline is the crisis point. When a task takes 12 months to complete, specialization commands a premium. When it takes three days, specialization becomes a liability. You are slow, expensive, and risk-averse. The commodity producer is fast, cheap, and already shipping.

Where Domain Specificity Becomes Irreplaceable

Satellite imagery is global. Foundation models are global. But Malaysia's regulatory and physical geography is specific. A flood risk map of the globe is worthless. A flood risk map that integrates:

- Satellite flood extent detection (foundation model layer)

- JPS (Department of Irrigation and Drainage) drainage basin boundaries and flood history

- JPPH (Department of Valuation and Property Services) property records and land-use classifications

- BNM (Bank Negara Malaysia) concentration data for insurance exposure in high-risk areas

- PDPA-compliant audit trail (required for regulatory sign-off)

That is proprietary. That is sticky. That is defensible.

Only if you layer domain-specific regulation and context on top of the foundation model. The model itself is commodity. The integration is proprietary.

For property valuers, the timing is crucial. The current window to integrate satellite imagery and computer vision into valuation pipelines is 6 to 12 months. After that window closes, foundation model efficiency means every competitor has the same capability. The firms that move first build the workflow. The firms that follow adopt the workflow. The firms that wait vanish.

For valuation workflows specifically: satellite flood extent mapping, rainfall intensity data, and JPS historical submergence records together produce a climate risk adjustment. That adjustment is now quantifiable in weeks, not months. For a property in Kuala Lumpur or Shah Alam, the climate risk premium becomes visible, standardized, and defensible in valuation reports. The first firm to systematize this owns the market. The second firm catches up. The third firm becomes a utility.

This is the same pattern I described in The Self-Sustaining Handoff: proprietary workflows are only defensible when they encode context that is hard to replicate, not when they optimize a process that is already commoditizing.

The Accounting Perspective: Who Bears the Cost of Commoditization?

Foundation model democratization compresses costs for everyone equally. But it compresses them unevenly across firm layers. The cost of model development falls 90 percent. The cost of data acquisition falls 70 percent. The cost of infrastructure falls 80 percent. But the cost of regulatory integration, domain expertise, and compliance auditing falls maybe 20 percent.

This means the cost structure of a geospatial firm shifts. What was once 60 percent data and model cost, 40 percent domain integration becomes 15 percent data and model cost, 85 percent domain integration. The profit margins of the first type of firm collapse. The margins of the second type stabilize or grow.

The trap: firms organized to win in the old cost structure will not adapt fast enough. They have too much sunk cost in data teams and model infrastructure. They have too much organizational inertia around "data processing excellence." They will cut satellite data costs 30 percent, celebrate the efficiency, and miss that they have become a utilities operator instead of an intelligence firm.

The firms that thrive are the ones that were already hybrid. Firms that integrated satellite data with regulatory databases. Firms that had domain experts interpreting models, not building them. Firms that saw foundation models coming and retrained their teams around "What does regulatory context plus satellite data tell us?" instead of "How do we process satellite data more efficiently?"

Six to Twelve Months to Adapt

Foundation models will reach the same efficiency curve that DNN image classification reached three years ago: so efficient that the task is essentially free, and the only differentiation is context. For geospatial firms, that timeline is tight.

The actions that win:

1. Move upstream in the stack. Stop building satellite data pipelines. Start building regulated domain models: flood risk combined with property finance, crop health combined with agricultural lending, urban expansion combined with infrastructure planning.

2. Integrate regulated data. In Malaysia, this means JPS, JPPH, BNM, PDPA-compliant audit trails. Make the combination so specific to the regulatory regime that nobody else can easily replicate it.

3. Hire domain experts, not model engineers. A domain expert who can interpret satellite data through the lens of JPS hydrology or JPPH valuation standards is now more valuable than a model engineer. The models are free. The interpretation is not.

4. Build for regulatory adoption. A flood-risk model is worthless until BNM accepts it, insurers price it, and property valuers can defend it in court. The technical capability is table stakes. The regulatory pathway is the moat.

The How I Run 0→1 Product Sprints principle applies here: the bottleneck is never the technology. It is the regulatory integration, the domain context, and the workflow that makes the technology meaningful to the specific market.

The Opportunity Is Real, But the Window Is Closing

When Meta released the tree-height map, the internet celebrated "democratizing geospatial intelligence." And it is true: the commodity layer is now freely accessible. But democratization is always a Trojan horse. The technology that democratizes the work you are doing simultaneously devalues the expertise you have built around it.

For geospatial firms, the real opportunity is not in celebrating the democratization. It is in recognizing it as the moment the competitive landscape shifted. The winners are not the ones who adopt foundation models fastest. They are the ones who layer domain-specific intelligence so deep, so integrated with local regulation and context, that a foundation model becomes just another input to a much larger system.

In Malaysia, for property finance and climate risk, that system is already taking shape. The firms building it now will own the market in 18 months. The firms waiting to see how foundation models mature will be too late.

The trap is real. But it is also avoidable. You have to move upstream before everyone else figures out they need to.

Strategy and technology are the same decision. Over 15 years in fintech (CTOS, D&B), prop-tech (PropertyGuru DataSense), and digital startups, I have built frameworks that help founders and executives make both moves at once. Based in Kuala Lumpur.

Working on a 0→1 product?

I help founders and operators go from idea to validated product. Let's talk about yours.

Get in touch →